We need your help! Join our growing army and click here to subscribe to ad-free Revolver. Or give a one-time or a recurring donation during this critical time.

When it comes to drinking coffee on the go, most people immediately think of Starbucks. Even if you’re not a coffee lover, Starbucks has managed to weasel it’s way into our collective consciousness, which, love them or hate them, is a powerful testament to their global branding. As it stands now Starbucks operates roughly 34,000 stores worldwide, and they are the Goliath of the coffee world. But what if we told you that Starbucks is a lot more than a coffee joint? And no, we’re not talking about soups and sandwiches. We’re talking about banking…

That’s right—one business and finance prodigy by the name of Brandon Teo says that Starbucks is actually operating as a bank. Teo has studied Starbucks closely, and he says that they operate with the financial prowess of a banking institution. But curiously, the company has never signaled any intentions to get into the banking industry.

So, what’s the story behind Starbucks being a “secret bank”? Well, to begin to unravel this java mystery, we need to remember exactly how a bank works. Most of us realize what banks do. They’re a safe place where people and businesses put their money. The bank then pays a little extra “thank you” money to customers who store their money there. In order to make money, the bank lends some of that stored money to others and charges them a bit more in loan fees. Banks also invest the money in stocks, bonds, or property to make even more money. So, based on those principles, Mr. Teo reveals how Starbucks is actually operating as a “secret bank” by using their customer rewards program.

As a Starbucks customer, you might have come across its loyalty program called Starbucks Rewards. If you’re new to how it works, you can add money into your Starbucks Rewards account via a credit card or Starbucks gift cards. The prepaid funds in the app can then be used to make payments to earn loyalty points (known as Stars) which can then be redeemed for complimentary food/drinks or discounts.

Mr. Teo points out that Starbucks has 27.4 million active members in its Rewards program in the U.S., which is nearly double the number from 2017. These members spend three times more than non-members, and in 2022, they make up over half (53%) of Starbucks’ revenue in U.S. stores. The Fifth Person piece goes on:

Within the customer loyalty space, Starbucks has consistently been credited with having one of the best rewards programs with a loyal customer following. Because of the company’s reputation, customers are not afraid to keep money in their Starbucks account, knowing that they can use it anytime. In fact, in its Q3 2022 earnings report, Starbucks reported that it had US$1.7 billion loaded on Starbucks accounts/gift cards waiting to be spent in its stores.

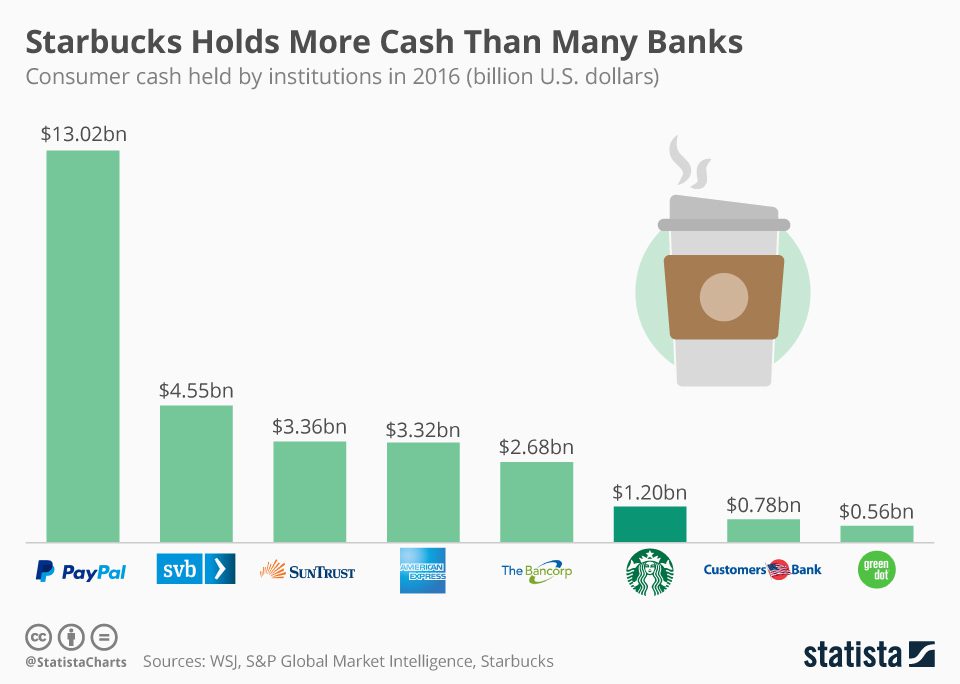

Starbucks is actually holding more money than most banks do. Mr. Teo goes on:

Just like how a bank collects cash deposits from its customers, Starbucks collects large amounts of cash from its members through its loyalty program. Interestingly, this amount is greater than the cash held by some banks. In 2016, Starbucks held US$1.2 billion in customer deposits, higher than banks like Customers bank and Green Dot which held US$0.78 billion and US$0.56 billion respectively.

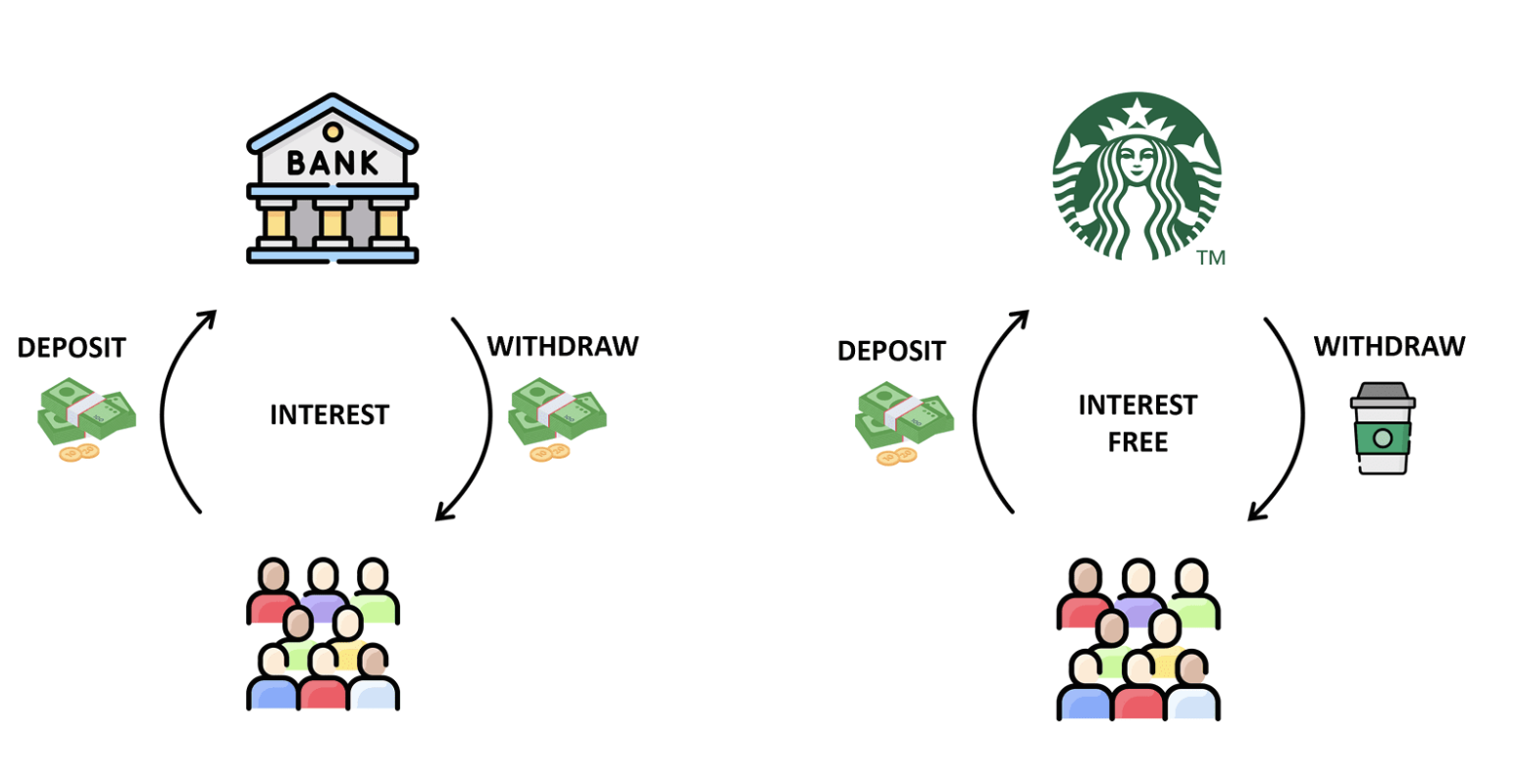

However, there’s one very big difference between Starbucks and a real bank. Real banks have to pay interest on customer deposits, Starbucks does not. As Mr. Teo so brilliantly puts it, Starbucks members effectively provide the company with a US$1.7-billion loan at zero percent interest.

Additionally, Starbucks earns a profit from breakage — the amount that is unused from gift cards every year. This amounted to around US$164.5 million in 2021 or around 10% of all stored value balances. So not only does Starbucks get an ‘interest-free loan’ from its members, but it also earns a roughly 10% return based on breakage!

What’s even better is that as opposed to a bank where customers can withdraw money anytime, Starbucks members can only withdraw coffee. This essentially locks in customers the moment they transfer funds into their Starbucks Rewards account, providing guaranteed revenue for Starbucks.

Mr. Teo’s discovery is indeed intriguing and a testament to his financial expertise. He also goes on to explains that Starbucks uses these funds for “working capital.” According to Mr. Teo, Starbucks isn’t engaging in any illegal activities, but they’ve certainly uncovered a loophole in the system. If news of this spreads, one can’t help but wonder if the banking industry will find some way to close that loophole very quickly.

We encourage you to check out Mr. Teo’s article in its entirety. You can find it by clicking here.

SUPPORT REVOLVER — DONATE — SUBSCRIBE — NEWSFEED — GAB — GETTR — TRUTH SOCIAL — TWITTER

Join the Discussion